A high credit score doesn’t guarantee financial efficiency. Millions of Americans unknowingly lose hundreds of dollars every year due to a single banking mistake: leaving their everyday money in outdated, poorly optimized bank accounts. This in-depth guide explains how hidden fees, low interest rates, and default bank settings quietly drain money—and how to fix the problem quickly and safely.

Why Having a Great Credit Score Isn’t Enough Anymore

For decades, personal finance advice has revolved around one central goal: build and protect your credit score. And to be fair, a strong credit profile does unlock meaningful benefits—lower loan rates, better credit card offers, and easier approvals.

But here’s the uncomfortable reality most banks don’t openly discuss: a great credit score does not prevent you from losing money through everyday banking.

In fact, many people with credit scores above 750 are losing more money annually than those with average credit—simply because they assume they are financially “set.”

The biggest financial leaks today don’t come from missed payments or bad credit decisions. They come from how your money sits, moves, and sleeps inside your bank accounts.

The One Banking Mistake That Costs Even Smart People Hundreds

The Mistake: Leaving Your Money in the Wrong Bank Accounts

The most damaging mistake is not reckless spending or debt—it’s using default checking and savings accounts that quietly work against you.

This usually includes:

- Savings accounts earning near-zero interest

- Checking accounts with hidden or conditional fees

- Poor overdraft configurations

- Missed fraud protections

- Lost rewards and benefits

Banks depend on customer complacency, and customers with great credit tend to be the most complacent of all.

Why This Mistake Is So Common Among “Financially Responsible” People

People with strong credit profiles often:

- Trust their bank without question

- Stay with the same institution for decades

- Prioritize convenience over optimization

- Assume fees don’t really apply to them

Ironically, banks make more predictable profits from these customers because they rarely complain or switch.

According to the FDIC, the average U.S. household loses over $250 per year in avoidable bank fees and lost interest—even without overdrafting.

How This Single Mistake Quietly Drains Your Money

1. The Low-Interest Savings Trap

Most traditional banks still offer savings accounts paying 0.01% to 0.05% APY. Meanwhile, inflation has averaged 3%–5% in recent years.

That gap is not harmless—it’s destructive.

Real-life example:

Michael, an engineer with a 790 credit score, kept $25,000 in a traditional savings account earning 0.04%. Over one year, he earned about $10 in interest. That same money in a high-yield savings account earning 4.5% would have generated over $1,100.

His credit score didn’t protect him.

His bank choice cost him.

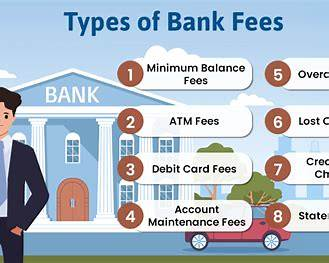

2. “Invisible” Checking Account Fees

Many checking accounts quietly charge:

- Monthly maintenance fees

- Minimum balance penalties

- ATM fees

- Paper statement fees

- Excess transaction fees

Individually, these charges seem small. Over a year, they easily add up to $150–$300—often unnoticed.

Even premium accounts often waive fees only if strict conditions are met.

3. Overdraft Settings Designed for Bank Profit

Even high-income, well-organized individuals overdraft occasionally—especially with:

- Auto-renewing subscriptions

- Delayed transaction posting

- Weekend or holiday charges

The problem isn’t overdrafting once.

The problem is leaving overdraft settings untouched.

With average overdraft fees around $35 per incident, one or two mistakes can erase months of interest earnings.

Banks generate billions annually from overdraft fees alone.

4. Using Debit Cards Instead of Credit Cards

Many financially responsible people rely heavily on debit cards to “avoid debt.”

Ironically, this costs them money.

Debit cards:

- Offer weaker fraud protection

- Pull funds directly from your account

- Do not earn rewards

- Can take weeks to resolve disputes

Credit cards—when paid in full—offer:

- Stronger fraud protection

- Cash back or points

- Grace periods

- Purchase insurance

By avoiding credit cards entirely, many people lose hundreds per year in rewards and protections.

5. Missing Out on Modern High-Yield Options

Fintech banks and cash-management platforms now offer:

- 4%–5% APY

- No minimum balances

- No monthly fees

- FDIC insurance via partner banks

Yet millions still keep large balances earning almost nothing—simply because they never revisit their setup.

This is one of the most expensive forms of financial inertia.

Why Banks Don’t Proactively Warn You

Banks benefit when:

- Money sits idle

- Customers don’t compare options

- Fees remain unnoticed

- Accounts stay unchanged

High-credit customers are especially profitable because they are perceived as “low maintenance.”

This is not a conspiracy—it’s a business model.

The Psychology That Keeps This Mistake Alive

This mistake persists due to:

- Status quo bias (sticking with what’s familiar)

- Trust inertia (believing big banks act in your best interest)

- Credit overconfidence (assuming a good score equals optimization)

In reality, credit scores measure borrowing behavior—not banking efficiency.

How to Fix This Mistake Without Complicating Your Life

You don’t need dozens of accounts or advanced financial tools.

Simple, practical steps:

- Keep only spending money in checking

- Move savings to a high-yield account

- Disable overdraft fees or link protection accounts

- Use credit cards for purchases and pay in full monthly

- Review bank fees once per year

These steps alone can save hundreds to thousands of dollars over time.

What a Smarter Banking Setup Looks Like Today

A modern setup typically includes:

- One fee-free checking account

- One high-yield savings or cash-management account

- One primary rewards credit card

- Automatic alerts and transaction monitoring

This is not about complexity—it’s about intentional design.

Why This Matters More During Economic Uncertainty

When inflation rises and interest rates fluctuate:

- Idle cash loses value faster

- Fees hurt more

- Missed interest compounds

The cost of this mistake grows every year you ignore it.

Key Takeaways

- A great credit score doesn’t protect you from bad banking

- The biggest losses come from low-interest, high-fee accounts

- Banks profit from customer inertia

- Small optimizations can save hundreds annually

- Modern banking tools make switching easier than ever

Frequently Asked Questions (Trending & Search-Optimized)

1. Can you lose money even with an excellent credit score?

Yes. Fees and lost interest impact everyone, regardless of credit score.

2. How much do people lose from low-interest savings accounts?

Often hundreds per year, depending on balances and inflation.

3. Are traditional banks bad for savings?

Many offer extremely low APYs compared to online and fintech banks.

4. Is it risky to use online or fintech banks?

Most are FDIC-insured through partner banks and meet regulatory standards.

5. Does switching banks hurt your credit score?

No. Bank accounts do not affect your credit score.

6. Why do banks still charge maintenance fees?

Because many customers don’t switch, and fees remain profitable.

7. Are debit cards less safe than credit cards?

They generally offer weaker fraud protection and slower dispute resolution.

8. How often should you review your bank accounts?

At least once per year or whenever rates and fees change.

9. Is keeping all money in one bank a bad idea?

Not always, but separating spending and savings often improves returns.

10. What’s the fastest way to fix this mistake?

Move idle cash to a high-yield account and review fee structures.

Final Thought

The most expensive financial mistakes today are not dramatic—they’re quiet.

They hide in outdated accounts, default settings, and the assumption that a great credit score means everything is optimized.

Fixing this one banking mistake is often the simplest—and fastest—way to keep more of your money working for you.

: A Smart Bet in America’s Housing Crunch")