The Federal Reserve’s next interest-rate decision could have consequences far beyond the stock market. From housing and employment to banking stability and global capital flows, monetary policy is now influencing every layer of the economy. This article explores why the Fed is cornered, what risks investors and households are underestimating, and how everyday Americans may feel the impact long after markets react.

Introduction: Why This Fed Decision Feels Unusually Dangerous

Every Federal Reserve meeting carries weight, but some moments carry gravity. This is one of them.

After the most aggressive interest-rate hiking cycle in over 40 years, the U.S. economy is no longer responding in neat, predictable ways. Inflation has cooled from its peak but remains uneven. Growth has slowed, but not collapsed. Employment remains strong on the surface, yet hiring momentum is weakening underneath. Credit stress is rising quietly, not explosively.

This places the Federal Reserve in an uncomfortable position.

Cut rates too soon, and inflation could return—damaging credibility and forcing harsher measures later. Hold rates too high for too long, and something else may break—banks, housing, employment, or global markets.

The danger is no longer limited to stocks. The Fed’s next decision could fracture parts of the financial system most Americans don’t watch—until they’re forced to feel it personally.

What Exactly Is the Fed Deciding Right Now?

At a high level, the Fed is deciding whether monetary policy should remain restrictive, ease slightly, or pivot more decisively. But underneath that technical framing lies a deeper dilemma.

The Fed must answer three difficult questions at the same time:

- Has inflation truly been defeated, or is it merely pausing?

- How much economic damage has already been baked in from past rate hikes?

- Where is the next point of financial stress most likely to emerge?

Interest rates operate with long and uneven lags. Historically, their full impact is often felt 12 to 24 months after hikes occur. That means the economy may still be absorbing the most painful effects—even if no new hikes happen at all.

This lag effect is why the next decision feels less like routine policy management and more like risk containment.

Why Stocks Are Only the Surface-Level Risk

Financial media tends to treat the stock market as the primary scoreboard. But focusing only on equity indices misses where real damage often starts.

Stocks are liquid, fast-moving, and reactive. Structural stress builds elsewhere first.

Areas under growing pressure include:

- Housing affordability

- Regional banking balance sheets

- Consumer credit

- Small business refinancing

- Global dollar-denominated debt

The stock market can fall and recover. Broken credit channels, lost jobs, or failed banks take much longer to heal.

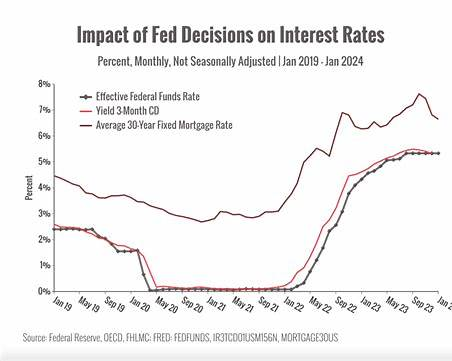

How the Fed’s Decision Could Reshape the Housing Market

One of the most common questions Americans are asking is:

“When will mortgage rates finally come down?”

Mortgage rates remain elevated not because housing demand is strong, but because monetary policy remains tight. This has created a frozen housing market:

- Existing homeowners won’t sell because they’re locked into low rates

- Buyers can’t afford monthly payments at current prices

- Builders face higher financing and labor costs

If the Fed holds rates higher for longer, affordability may deteriorate further—even if home prices stop rising. That hurts first-time buyers the most and deepens generational inequality.

If the Fed cuts too early, demand could spike again, pushing prices higher and reigniting shelter inflation. Either outcome carries pain.

Housing, once a stabilizer, has become one of the most fragile transmission channels of Fed policy.

Could the Fed Accidentally Break the Labor Market?

The labor market has remained resilient, but it is no longer accelerating.

Job openings are declining. Voluntary quits are down. Wage growth is slowing. Companies are cautious, not confident.

The Fed has openly acknowledged that labor conditions may need to cool to keep inflation under control. Translated into real life, that means:

- Slower hiring

- Fewer raises

- Reduced job mobility

- Higher risk for marginal workers

Employment tends to weaken late in the cycle, not early. That’s what makes this period dangerous. Once job losses accelerate, confidence can unravel quickly.

Why Banks Are Quietly Watching This Decision Closely

Bank stress never truly disappeared—it just moved off front pages.

Many banks still hold long-duration bonds purchased at low yields before rates rose. These assets carry unrealized losses. As long as deposits remain stable, those losses stay theoretical. But if confidence wavers, they become very real.

High interest rates increase pressure on banks by:

- Raising deposit costs

- Reducing loan demand

- Increasing default risk

- Tightening credit availability

The Fed knows that prolonged restriction raises systemic risk. Yet easing prematurely risks inflation resurgence.

This tradeoff—financial stability versus inflation control—is now central to every policy meeting.

The Global Consequences Most Americans Don’t See

Another increasingly common search query is:

“How does the Fed affect the global economy?”

The answer is: more than any other central bank.

When U.S. rates stay high:

- The dollar strengthens

- Capital flows out of emerging markets

- Dollar-denominated debt becomes harder to service

Many countries, corporations, and governments borrowed heavily in dollars during years of low rates. That debt is now far more expensive.

History shows that global stress often feeds back into U.S. markets through trade, financial contagion, and confidence channels. The Fed cannot fully insulate the U.S. from global consequences of its own policy.

Why Inflation Isn’t the Only Threat Anymore

For years, inflation dominated policy thinking. Today, the threat landscape is wider.

The risks now include:

- Asset deflation occurring unevenly

- Credit markets tightening without headlines

- Consumers relying more heavily on debt

- Corporate refinancing cliffs approaching

The danger is not a dramatic collapse—but a slow accumulation of stress that eventually reaches a breaking point.

Lessons from Past Fed Policy Mistakes

History doesn’t repeat exactly, but it often rhymes.

In past cycles, the Fed believed inflation was under control, only to see it return. In others, it underestimated how long rate hikes would take to damage growth.

A consistent lesson emerges:

The most severe consequences usually appear after policymakers believe the worst is over.

This is why market complacency is often misplaced during late-cycle policy periods.

What Everyday Americans Should Be Paying Attention To

Instead of obsessing over Fed press conferences, Americans should watch real-world signals.

Key indicators that matter more than headlines:

- Credit card delinquency rates

- Auto loan default trends

- Bank lending standards

- Small business loan availability

- Job openings relative to unemployment

These metrics often deteriorate before stock markets react meaningfully.

Practical Takeaways: How to Protect Yourself Now

You don’t need to predict the Fed perfectly to reduce risk.

Practical actions many households are considering:

- Maintaining larger emergency savings

- Avoiding unnecessary variable-rate debt

- Stress-testing monthly budgets

- Preserving career flexibility

- Prioritizing liquidity over speculation

Periods of policy transition reward caution, not bravado.

Why This Decision Feels Like a Tipping Point

The anxiety surrounding this Fed decision isn’t about imminent collapse. It’s about shrinking margins for error.

Debt levels are higher than in previous cycles. Political pressure is louder. Global coordination is weaker. Trust in institutions is thinner.

The Fed may succeed in avoiding catastrophe—but even success may involve tradeoffs that leave parts of the economy bruised.

Conclusion: More Than a Market Event

The Fed’s next decision will not simply move markets for a day or a week. It will shape credit conditions, employment prospects, housing affordability, and financial stability for years.

Stocks may react instantly. The real consequences will unfold slowly—often invisibly—until they can no longer be ignored.

Understanding this moment isn’t about predicting headlines. It’s about recognizing risk, managing exposure, and preparing for uncertainty in a world where policy decisions carry unusually high stakes.

Frequently Asked Questions (SEO-Optimized – 10 FAQs)

1. Why is the Fed’s next decision so important?

Because economic stress is building beneath the surface, and policy errors could trigger broader instability.

2. Will the Fed cut interest rates soon?

Possibly, but only if inflation and financial conditions allow it.

3. Could high rates cause a recession?

Yes, especially if credit tightens faster than incomes adjust.

4. How does the Fed affect regular Americans?

Through mortgage rates, job conditions, loan costs, and prices.

5. Are banks still at risk?

Some remain vulnerable due to bond losses and funding pressures.

6. What happens if the Fed cuts rates too early?

Inflation could return, forcing even harsher policy later.

7. Is the housing market going to crash?

A crash is unlikely, but prolonged affordability stress is likely.

8. How does this affect retirement accounts?

Volatility may increase, and bond values remain sensitive to rates.

9. Why does the global economy care about the Fed?

U.S. policy drives global capital flows and debt costs.

10. What risk are investors underestimating most?

That financial stress often emerges where models don’t predict it.