Wall Street is celebrating resilience, but history shows economic damage rarely appears when policy decisions are made. Instead, it emerges months—or even years—later through what economists call the “lag effect.” This article explains why markets consistently underestimate delayed consequences, how interest rate hikes ripple through jobs, housing, and credit, and what Americans should watch as hidden pressures build beneath today’s calm surface.

Introduction: Why the Market’s Calm Should Make You Nervous

Markets feel surprisingly calm.

Stocks hover near highs. Volatility is muted. Headlines suggest the economy has absorbed higher interest rates better than expected. Many investors are already talking about soft landings, avoided recessions, and the next growth cycle.

But experienced investors and economists know something unsettling: this is often what the most dangerous phase looks like.

Economic history is filled with moments when conditions appeared stable right before things broke. Not because policy changes failed—but because their effects hadn’t arrived yet.

This delayed reaction is known as the lag effect, and it has repeatedly blindsided Wall Street. Today, the risk isn’t what the Federal Reserve has already done. It’s what hasn’t shown up yet.

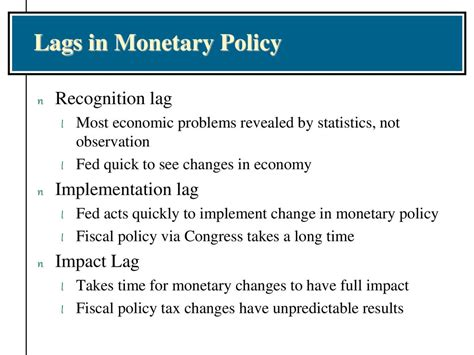

What Is the Lag Effect? (Plain English Explanation)

The lag effect refers to the time delay between economic actions and their real-world consequences.

When interest rates rise, the impact is not immediate. Borrowers don’t default overnight. Businesses don’t cancel expansion plans instantly. Consumers don’t suddenly stop spending the next day.

Instead, effects emerge gradually:

- Loans reset when promotional or fixed-rate periods end

- Businesses refinance debt at higher costs months later

- Hiring slows before layoffs appear

- Credit conditions tighten quietly before defaults rise

This delay creates a false sense of security. Things look fine—until they’re not.

Why Wall Street Keeps Underestimating the Lag Effect

Wall Street is designed for speed. The lag effect works on patience.

Markets price news instantly, but economic damage unfolds slowly. This mismatch causes investors to declare victory too early.

Common reasons the lag effect is underestimated:

- Markets focus on current data, not delayed consequences

- Financial models assume past cycles repeat cleanly

- Short-term resilience is extrapolated into long-term safety

- Psychological bias favors recent good news

The result is a dangerous pattern: confidence rises precisely when risks are still accumulating.

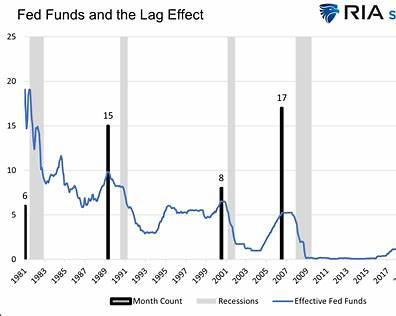

How Long Does the Lag Effect Actually Take?

One of the most common questions Americans are asking is:

“How long do interest rate hikes take to affect the economy?”

Historical data and Federal Reserve research suggest:

- Consumer spending effects: 6–12 months

- Business investment slowdown: 9–18 months

- Labor market weakening: 12–24 months

- Credit defaults and bankruptcies: 18–36 months

This means much of the economic impact from recent tightening may still be ahead, not behind us.

A Real-World Example: The Illusion of 2006–2008

In 2006, the U.S. economy looked healthy.

- Home prices were rising

- Unemployment was low

- Corporate profits were strong

Yet the Federal Reserve had already raised rates significantly.

The lag effect unfolded quietly:

- Adjustable-rate mortgages began resetting

- Delinquencies rose slowly

- Credit markets tightened beneath the surface

By the time markets reacted, the damage was irreversible. The crisis didn’t begin when rates were raised—it began when the lag finally caught up.

Why Today’s Lag Effect May Be More Dangerous

Today’s economy is structurally different—and more fragile.

Factors amplifying today’s lag effect:

- Higher household and corporate debt levels

- Greater reliance on variable-rate credit

- More leveraged financial systems

- Faster sentiment shifts driven by technology

Consumers are carrying record credit card balances. Businesses face refinancing cliffs. Governments are servicing historically high debt at rising interest rates.

When lag effects hit multiple sectors simultaneously, the consequences compound.

Where Lag Effects Usually Appear First (Hint: Not Stocks)

Lag effects rarely show up in stock indices first. They appear where fewer people are watching.

- Credit card delinquency rates

- Auto loan defaults

- Small business closures

- Bank lending standards

- Temporary hiring freezes

By the time these pressures hit markets, the real economy has often been deteriorating for months.

This is why market calm can be misleading.

Why the Job Market Isn’t as Safe as It Looks

Another popular question Americans are asking:

“Why is the job market still strong if rates are high?”

Because employment is a lagging indicator.

Companies don’t lay off workers immediately. They first:

- Reduce job postings

- Delay expansion plans

- Cut bonuses

- Freeze hiring

Layoffs come later—and when they do, confidence drops fast.

Historically, unemployment rises after economic slowdowns begin, not before.

Housing and the Slow-Burning Lag Effect

Housing absorbs rate hikes slowly but painfully.

- Homeowners with low-rate mortgages don’t sell

- Buyers hit affordability ceilings

- Builders delay new projects

- Inventory stagnates

Instead of crashing, housing freezes. But prolonged freezes create secondary damage:

- Reduced labor mobility

- Slower construction employment

- Declining local tax revenues

Housing stress from lag effects is subtle—until it becomes systemic.

Corporate Debt: The Lag Effect Time Bomb

One of the least discussed risks is corporate refinancing.

Many companies borrowed heavily during ultra-low-rate years. That debt matures gradually.

As refinancing occurs:

- Interest expenses rise

- Profit margins shrink

- Hiring slows

- Investment declines

Defaults don’t spike overnight. They rise slowly—then suddenly.

Lag effects mean today’s earnings can look strong while tomorrow’s balance sheets weaken.

Wall Street’s Favorite Mistake: Declaring “Soft Landings” Too Early

Markets love narratives, and the most popular one today is the soft landing.

History shows soft landings are rarely obvious in real time. They’re confirmed only years later—after no hidden damage emerges.

Premature optimism often leads to:

- Overconfidence

- Excessive risk-taking

- Ignoring early warning signs

The lag effect punishes certainty before outcomes are known.

Practical Signs the Lag Effect Is Accelerating

Instead of watching headlines, watch behavior.

Early warning signs include:

- Rising minimum payments on consumer debt

- Banks tightening lending standards

- Declining small business optimism

- Fewer full-time job openings

- Increased withdrawals from savings

These signals often worsen quietly before markets react.

What This Means for Everyday Americans

The lag effect isn’t just a Wall Street issue.

As delayed impacts spread:

- Credit becomes harder to access

- Job security weakens

- Housing options narrow

- Emergency savings become critical

Many households feel financial stress without understanding why—because the cause happened months or years earlier.

Practical Steps to Prepare for Lag Effects

You don’t need perfect predictions. You need resilience.

Practical actions many Americans are taking:

- Increasing emergency savings

- Avoiding unnecessary variable-rate debt

- Stress-testing monthly budgets

- Preserving career flexibility

- Prioritizing liquidity over speculation

Preparation matters most before lag effects become obvious.

The Psychological Trap of Lag Effects

Humans anchor to recent experience.

When markets hold up, we assume stability. When jobs remain plentiful, we expect security. Lag effects exploit that bias.

By the time fear replaces confidence, options narrow.

Understanding lag effects is less about fear—and more about timing.

Final Thoughts: The Danger Isn’t the Hike—It’s the Delay

The most dangerous phase of an economic cycle is not when policy tightens, but when people believe tightening no longer matters.

The lag effect is invisible until it isn’t. Wall Street underestimates it not because it’s unknown, but because it’s uncomfortable.

History doesn’t punish caution too early.

It punishes confidence too late.

Frequently Asked Questions (10 SEO-Optimized FAQs)

1. What is the lag effect in economics?

It’s the delay between policy actions and their real-world economic consequences.

2. How long do interest rate hikes take to affect the economy?

Typically 12–24 months, sometimes longer.

3. Why doesn’t the stock market react immediately?

Markets price expectations, not delayed outcomes.

4. Is the lag effect happening now?

Evidence suggests many effects are still unfolding.

5. Why is employment still strong?

Jobs are a lagging indicator that weakens later.

6. Does the lag effect always cause recessions?

Not always, but it significantly increases downside risk.

7. How does the lag effect affect consumers?

Through credit costs, job security, and spending power.

8. Why do investors underestimate lag effects?

Short-term focus and psychological bias.

9. What sectors are most vulnerable to lag effects?

Credit, housing, small businesses, and leveraged companies.

10. What’s the best defense against lag effects?

Liquidity, flexibility, and disciplined risk management.