Cryptocurrency is no longer operating outside the U.S. financial system. Instead of disrupting banks, digital assets are being quietly integrated into them through fintech platforms, stablecoins, tokenized deposits, and blockchain infrastructure. This in-depth article explains how crypto and fintech are merging within American banking, why it’s happening now, and what it means for consumers, regulators, and the future of money.

Introduction: The Financial Shift Most Americans Haven’t Noticed

For more than a decade, cryptocurrency was portrayed as an outsider—an alternative financial system built to bypass banks, governments, and traditional institutions. Early adopters spoke of decentralization and financial freedom, while regulators and banks warned of volatility, scams, and instability.

Yet in 2025, something far more subtle—and arguably more powerful—is happening.

Crypto didn’t overthrow the U.S. banking system.

It quietly merged with it.

Today, blockchain technology and digital assets are being woven into the fabric of American finance through fintech apps, institutional banking tools, and payment infrastructure. Most consumers never see the word “crypto” on their screens, yet they benefit from faster payments, lower costs, and new financial products powered by the very technology once considered disruptive.

This is not a loud revolution.

It’s a silent transformation.

What the “Crypto-Fintech Fusion” Actually Means

The crypto-fintech fusion refers to the integration of digital assets, blockchain networks, and crypto-based infrastructure into regulated financial services, often without direct consumer exposure to cryptocurrency itself.

This fusion rarely looks like buying Bitcoin at a bank branch.

Instead, it appears as:

- Fintech apps offering crypto alongside checking-style accounts

- Stablecoins used for settlement behind the scenes

- Tokenized deposits moving across blockchain rails

- Banks offering crypto custody to institutional clients

- Payments settling instantly instead of over several days

For the consumer, the experience feels familiar.

For the financial system, it represents a fundamental upgrade.

Why This Shift Is Happening Now

The timing of this fusion is not accidental. Multiple forces are converging at once.

Key drivers accelerating crypto-fintech integration:

- Consumer comfort with digital-first finance

- Demand for instant, 24/7 payments

- Competition from fintech-native platforms

- Pressure to modernize outdated banking rails

- Increasing regulatory clarity around digital assets

According to industry surveys, over 40% of U.S. adults have interacted with cryptocurrency in some form, whether through trading apps, payments, or investment exposure. Ignoring that reality is no longer an option for banks.

At the same time, fintech firms are pushing the limits of what traditional infrastructure can support—forcing collaboration rather than confrontation.

Real-Life Example: Crypto Without the “Crypto Moment”

Imagine sending money on a Sunday night using a fintech app. The funds arrive instantly. No waiting until Monday. No bank processing delays.

To the user, this feels like good design.

Behind the scenes, however, that transaction may be settling using:

- Stablecoins

- Blockchain-based clearing networks

- Tokenized bank liabilities

The user never sees a wallet address or blockchain explorer. Yet crypto infrastructure makes the speed possible.

This is the essence of the crypto-fintech fusion: digital assets powering finance invisibly.

How U.S. Banks Are Participating—Quietly

Publicly, many U.S. banks remain cautious about cryptocurrency. Privately, they are experimenting aggressively—within regulatory boundaries.

Most banks are not offering retail crypto trading. Instead, they focus on infrastructure and institutional services.

Common ways banks are integrating digital assets:

- Providing crypto custody for asset managers

- Using blockchain for internal settlement

- Piloting tokenized deposits and funds

- Partnering with regulated crypto infrastructure firms

This strategy allows banks to gain exposure and expertise without the reputational risks associated with speculative retail trading.

Fintech’s Unique Role as the Translator

Fintech companies serve as the bridge between innovation and usability.

Unlike traditional banks, fintech platforms are designed for rapid iteration and customer-centric experiences. They can introduce crypto-powered features without overwhelming users.

Examples of fintech-led crypto integration:

- Buying and holding digital assets inside payment apps

- Using stablecoins for cross-border transfers

- Offering yield products backed by blockchain settlement

- Embedding tokenized assets in digital wallets

For users, these feel like fintech upgrades—not crypto experiments.

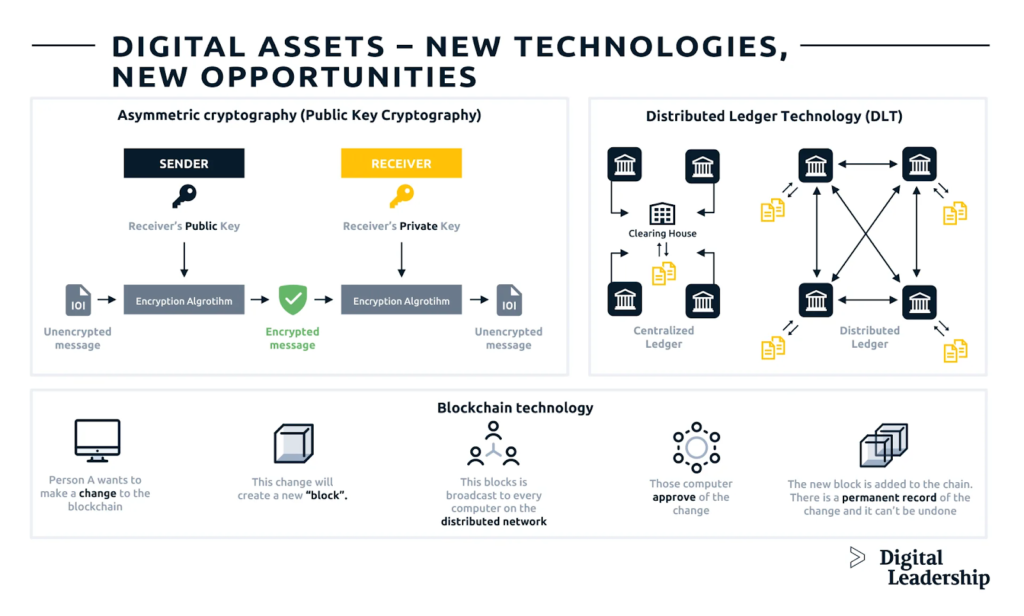

Stablecoins: The Backbone of Quiet Adoption

If Bitcoin introduced the world to crypto, stablecoins are introducing crypto to banking.

Stablecoins are digital tokens pegged to stable assets like the U.S. dollar. They combine blockchain efficiency with price predictability, making them ideal for payments and settlement.

Why stablecoins matter to banks and fintechs:

- Near-instant settlement

- Reduced counterparty risk

- Lower transaction costs

- Programmable payment features

- Compatibility with existing compliance systems

In many cases, stablecoins function as digital cash equivalents, moving value faster than traditional banking rails ever could.

Tokenization: When Traditional Assets Go Digital

Tokenization is one of the most important—and least understood—developments in modern finance.

It involves representing real-world assets, such as deposits, bonds, or funds, as digital tokens on a blockchain.

Benefits of tokenization include:

- Faster settlement times

- Reduced operational complexity

- Fractional ownership opportunities

- Improved transparency

Major financial institutions are already piloting tokenized money-market funds and bank deposits, signaling that tokenization is not experimental—it’s inevitable.

Regulation: Why the Fusion Looks So Quiet

One reason the crypto-fintech merger lacks drama is regulation.

U.S. banks and fintech firms operate under strict rules governing:

- Customer protection

- Anti-money laundering

- Capital requirements

- Custody standards

Rather than bypassing these rules, most institutions are choosing compliant integration. This slows adoption—but makes it durable.

The result is progress without spectacle.

Are Banks Rejecting Crypto or Refining It?

Some critics argue banks are embracing blockchain while rejecting crypto. The truth lies in the middle.

Banks are cautious about:

- Highly volatile tokens

- Unregulated exchanges

- Retail speculation risk

But they are increasingly comfortable with:

- Stablecoins

- Tokenized deposits

- Permissioned blockchains

- Regulated digital assets

This is not rejection—it’s selective adoption.

What This Means for Everyday Americans

Most consumers will not wake up one day to “crypto banking.”

Instead, changes will arrive gradually:

- Faster payments

- Lower fees

- More flexible financial products

- Greater access to digital tools

You may never own cryptocurrency directly, yet benefit from the infrastructure it introduced.

Common Consumer Concerns—and Why They Matter

Despite growing adoption, skepticism remains.

Common pain points include:

- Fear of hacks or lost funds

- Confusion over crypto terminology

- Regulatory uncertainty

- Trust in new financial systems

Banks and fintech firms are responding by emphasizing insurance, education, and strong user protections.

Trust—not technology—is the real bottleneck.

Is Crypto Losing Its Original Vision?

Some early crypto supporters worry that institutional adoption undermines decentralization.

From a consumer perspective, however, institutional involvement often signals legitimacy and safety.

The fusion represents a compromise:

- Less ideological purity

- More real-world usability

For most Americans, that trade-off feels worthwhile.

Where This Is Headed Next

Experts expect crypto to continue moving deeper into financial infrastructure rather than consumer hype.

Likely future developments:

- Tokenized bank deposits

- Blockchain-based interbank settlement

- Stablecoins embedded in payments

- Crypto custody becoming standard for institutions

Crypto won’t replace banks.

It will redefine how banks operate.

Final Takeaway: A Silent Financial Upgrade

The crypto-fintech fusion is not about overthrowing the financial system—it’s about upgrading it.

Digital assets are entering U.S. banking through collaboration, regulation, and infrastructure—not rebellion.

For consumers, the biggest changes may be invisible—but profoundly impactful.

Frequently Asked Questions (SEO-Optimized)

1. Are U.S. banks using cryptocurrency today?

Yes. Many banks use crypto-related infrastructure like custody and tokenization.

2. Can I buy crypto directly from my bank?

Some banks offer limited access indirectly, often via partnerships.

3. What role do stablecoins play in banking?

They enable fast, low-cost settlement and payments.

4. Is blockchain being used without crypto?

Yes, but often alongside regulated digital assets.

5. Are fintech apps safer than crypto exchanges?

Generally yes, due to stricter regulation and oversight.

6. Will crypto replace traditional banking?

Unlikely. Integration is more realistic than replacement.

7. Are tokenized assets safe?

Safety depends on regulation, custody, and provider quality.

8. Is crypto regulated in the U.S.?

Partially. Regulation is evolving and fragmented.

9. Why is adoption happening quietly?

Institutions prioritize stability and trust over hype.

10. What should consumers watch next?

Stablecoins, tokenization, and crypto custody services.

")