Inflation may feel invisible, but its effects on savings are real and potentially devastating. In 2026, even modest inflation rates could quietly erode the purchasing power of your money, making your hard-earned savings worth less over time. Understanding this “silent inflation factor” and taking strategic action can protect your financial future and help your money grow in real terms.

Understanding the Silent Inflation Factor

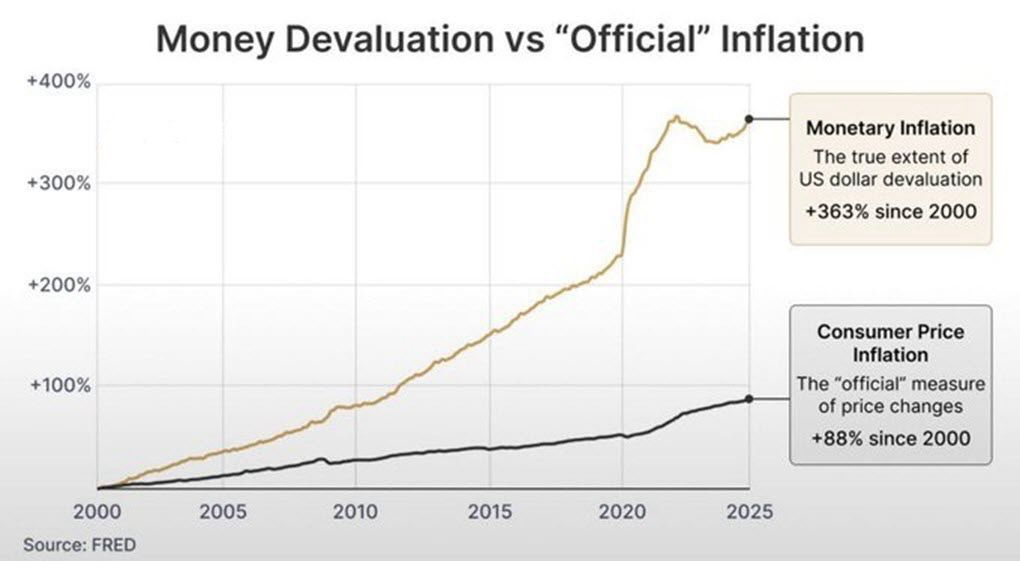

Inflation isn’t just a headline number. It’s the gradual erosion of money’s purchasing power over time. While high inflation grabs attention, the real danger comes from smaller, persistent increases in prices that quietly reduce the value of cash holdings, savings accounts, and low-yield investments.

For example, consider this: if you have $100,000 in a savings account earning 2% interest annually, but inflation is running at 3%, your money’s real purchasing power is shrinking by 1% every year. Over 5 years, that seemingly safe balance will lose about 5% of its value, even if the nominal balance grows.

Real-life evidence from past decades demonstrates the danger:

- In the 1970s and early 1980s, inflation rates often exceeded 10%, and many retirees found their savings rapidly losing value despite careful planning.

- In the 2020s, ultra-low interest rates compounded the problem, as bank savings accounts failed to keep pace with even modest inflation, leaving millions of Americans with diminished purchasing power.

Why 2026 Could Be Especially Risky

Several factors make 2026 a year to watch:

- Persistent Core Inflation

Even if headline inflation appears moderate, core inflation (which excludes volatile food and energy costs) can silently increase, pushing up prices across essentials like healthcare, housing, and services. - Interest Rates Lagging Inflation

Savings accounts and low-risk investments often lag behind inflation, meaning real returns may be negative for extended periods. - Economic Recovery Volatility

As the U.S. economy navigates post-pandemic recovery and shifting monetary policy, market volatility could exacerbate inflationary pressures. - Global Supply Chain Issues

Disruptions in supply chains for goods and raw materials can lead to higher prices, further eating away at savings. - Rising Costs of Living

Healthcare, housing, and education costs are projected to outpace traditional savings returns, silently eroding wealth.

How Silent Inflation Works: Real-Life Examples

- Everyday Purchases

In 2021, the average cost of groceries in the U.S. rose by over 4% compared to the previous year. If a family spent $500 per month, that translates to an extra $20 monthly. Over time, this incremental increase quietly diminishes disposable income and savings potential. - Retirement Savings

A retiree with a fixed monthly withdrawal of $3,000 may find that after a few years of persistent inflation, this amount buys 10–15% less in goods and services, even if nominal dollars remain the same. - College Savings

Parents saving for college may see tuition rates rise faster than their investments, resulting in a funding gap that requires either higher contributions or delayed plans.

The Mechanics of Silent Inflation on Savings

Silent inflation impacts your finances in several subtle ways:

- Savings Accounts – Most traditional accounts provide low interest rates, often below the inflation rate, resulting in negative real returns.

- Certificates of Deposit (CDs) – While slightly higher-yielding, long-term CDs lock in returns that may fall short of inflation.

- Bonds – Fixed-income investments can lose value when interest rates rise or inflation accelerates.

- Cash Holdings – Money kept as cash in wallets or checking accounts loses value steadily without growth.

Protecting Your Savings: Practical Strategies

Even though silent inflation is stealthy, there are ways to safeguard your wealth:

1. Diversify Investments

- Spread savings across stocks, bonds, and inflation-protected assets.

- Consider Treasury Inflation-Protected Securities (TIPS) to maintain real returns.

2. Prioritize Real Return Over Nominal Return

- Focus on investments that beat inflation, not just grow in nominal dollars.

3. Reevaluate Savings Accounts

- Compare high-yield accounts or online banks to traditional banks.

- Ensure returns at least match inflation expectations.

4. Invest in Assets With Intrinsic Value

- Real estate, commodities, and dividend-paying stocks can provide protection against rising prices.

5. Regularly Adjust Financial Plans

- Monitor inflation trends and adjust savings contributions or investment strategies accordingly.

Frequently Asked Questions (FAQs)

1. What is silent inflation?

Silent inflation refers to the gradual erosion of your money’s purchasing power due to persistent price increases, often unnoticed in everyday life.

2. How does inflation affect my savings?

Inflation reduces the real value of cash and low-yield investments, meaning your money buys less over time.

3. Can a 2% savings account keep up with inflation?

No. If inflation exceeds 2%, the real purchasing power of your savings declines even if the nominal balance grows.

4. What investments protect against inflation?

TIPS, stocks, real estate, commodities, and certain dividend-paying investments typically help hedge against inflation.

5. Is inflation expected to rise in 2026?

Economic forecasts indicate moderate but persistent inflation may continue, particularly in housing, healthcare, and essential goods.

6. How can retirees protect themselves from inflation?

Retirees should diversify assets, consider inflation-protected investments, and adjust withdrawal rates based on cost-of-living increases.

7. Are CDs safe during inflation?

CDs are safe nominally, but they may not keep pace with inflation, resulting in negative real returns.

8. Does inflation impact all income levels equally?

No. Those on fixed incomes or with low savings are disproportionately affected because they have less flexibility to absorb rising costs.

9. Can budgeting alone protect against inflation?

Budgeting helps manage expenses but cannot counteract the loss of purchasing power in savings or investments.

10. How often should I review my savings strategy?

At least annually, or whenever inflation trends significantly change, to ensure your strategy maintains real value growth.

Key Takeaways

- Silent inflation is real and dangerous. Even modest rates can erode savings over time.

- Nominal gains don’t equal real gains. Always consider the purchasing power of your money.

- Diversification is essential. Assets that protect against inflation are crucial.

- Monitor economic trends. Early action prevents long-term loss.

")